FRESH Hacker News

Hacker News

Although I lack the maths to determine it numerically (depends on volatility etc.), it looks to me as though all six are overbetting and would be ruined in the long run. It would have been interesting to compare against a constant fraction portfolio that maintains 1/6 in each asset, as closely as possible while optimising for fees. (Or even better, Cover's universal portfolio, seeded with joint returns from the recent past.)

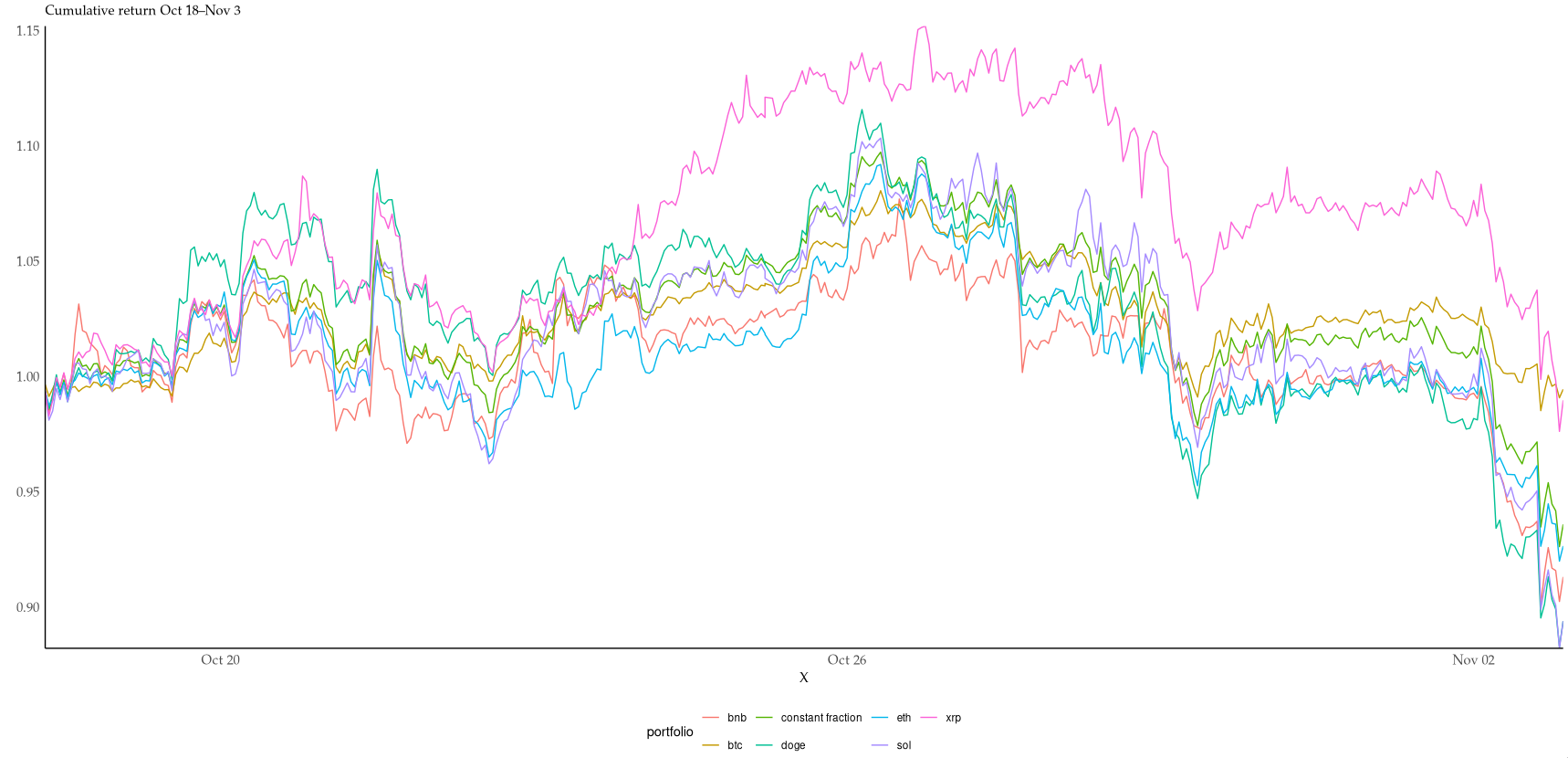

I couldn't resist starting to look into it. With no costs and no leverage, the hourly rebalanced portfolio just barely outperforms 4/6 coins in the period: https://i.xkqr.org/cfportfolio-vs-6.png. I suspect costs would eat up many of the benefits of rebalancing at this timescale.

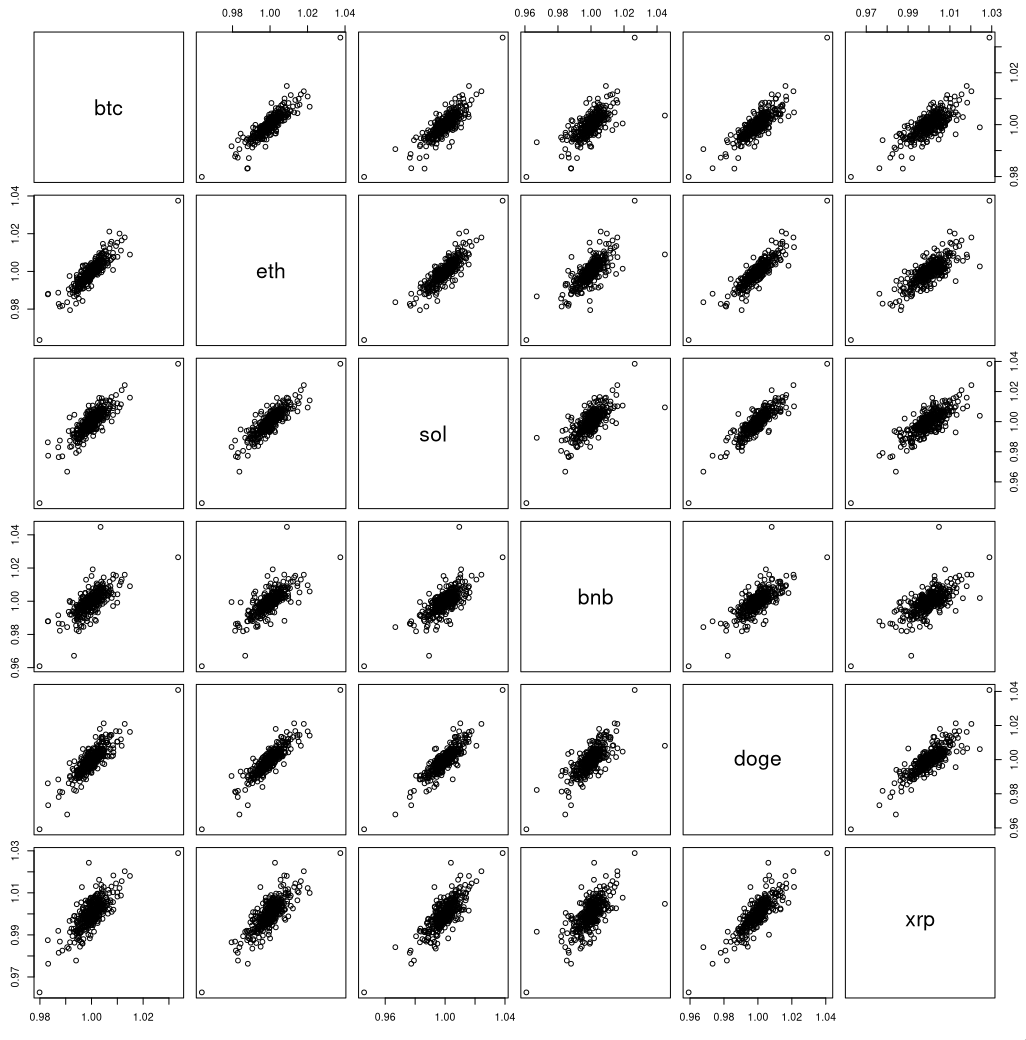

This is not too surprising, given the similiarity of coin returns. The mean pairwise correlation is 0.8, the lowest is 0.68. Not particularly good for diversification returns. https://i.xkqr.org/coinscatter.png

> difficulty executing against self-authored plans as state evolves

This is indeed also what I've found trying to make LLMs play text adventures. Even when given a fair bit of help in the prompt, they lose track of the overall goal and find some niche corner to explore very patiently, but ultimately fruitlessly.

You need domain knowledge to get this to work. Things like "we fed the model the market data" are actually non-obvious. There might be more than one way to pre-process the data, and what the model sees will greatly affect what actions it comes up with. You also have to think about corner cases, eg when AlphaZero was applied to StarCraft, they had to give it some restrictions on the action rate, that kind of thing. Otherwise the model gets stuck in an imaginary money fountain.

But yeah, the AI thing hasn't passed by the quant trading community. A lot of things going on with AI trading teams being hired in various shops.

And if you feeding or harnessing as the blog post puts it in a way that where it reasons things like:

> RSI 7-period: 62.5 (neutral-bullish)

Then it is no better than normal automated trading where the program logic is something along the lines if RSI > 80 then exit. And looking at the reasoning trace that is what the model is doing.

> BTC breaking above consolidation zone with strong momentum. RSI at 62.5 shows room to run, MACD positive at 116.5, price well above EMA20. 4H timeframe showing recovery from oversold (RSI 45.4). Targeting retest of $110k-111k zone. Stop below $106,361 protects against false breakout.

My understanding is that technical trading using EMA/timeframes/RSI/MACD etc is big in crypto community. But to automate it you can simply write python code.

I don't know if this is a good use of LLMs. Seems like an overkill. Better use case might have been to see if it can read sentiments from Twitter or something.

This kind of error just feels comical to me, and really makes it hard for me to believe that AGI is anywhere near. LLM's struggle to understand the order of datasets, when explicitly told. This is like showing a coin trick to a child, except perhaps even simpler.

A threshold in the single-digit milliseconds range allows the rapid detection of price reversals (signaling the need to exit a position with least loss) in even the most liquid of real futures contracts (not counting rare "flash crash" events).

Seems to me that the outcome would be near random because they are so poorly suited. Which might manifest as

> We also found that the models were highly sensitive to seemingly trivial prompt changes

But I also see this incredible growth curve to LLM's improvement. 2 years ago, I wouldn't expect llm's to one shot a web application or help me debug obscure bugs and 2 years later I've been proven wrong.

I completely believe that trading is going to be saturated with ai traders in the future. And being able to predict and detect ai trading patterns is going to be an important leverage for human traders if they'll still exist

Proves that LLM's are nowhere near close to AGI.

I don't think LLMs are anywhere close to "mastery" in chess or go. Maybe a nitpick but the point is that a NN created to be good at trading is likely to outperform LLMs at this task the same way way NNs created specifically to be good at board games vastly outperform LLMs at those games.

I've been following these for a while and many of the trades taken by DeepSeek and Qwen were really solid

In addition, I cannot imagine how the selection of securities was chosen. Is XRP seriously part of the proposed asset mix here?

It's hard not to look at this and view it as a marketing stunt. Nothing about the results are surprising and the setup does not seem to make any sense to me to begin with.

I use LLMs a lot and I work in finance and I don’t see how a LLM benefits in this space.

Also it looks like none of their data uses any kind of benchmarking. It’s purely a which model did better which I don’t think tells you much.

{kind=link}

{kind=link}